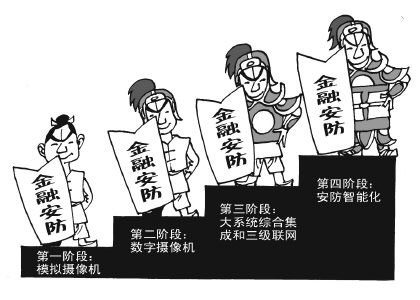

As China's "Safe City" initiative continues to expand into second- and third-tier cities, there's been a noticeable surge in global demand for similar public safety projects. Around the world, communities are increasingly relying on advanced security technologies and equipment, making these products more accessible and familiar to everyday life. The report titled "Market Analysis and Investment Direction Research Report for the Security Industry (2012-2016)" highlights that investments in China's urban intelligent transportation systems are projected to hit RMB 127.77 billion between 2012 and 2016, with over 70 billion yuan allocated specifically to video surveillance systems. That averages out to more than 10 billion yuan annually, reflecting the robust demand for security solutions across key domestic sectors.

Over time, China's security industry has evolved into three major regional clusters: the Pearl River Delta, known for its electronics manufacturing prowess; the Yangtze River Delta, home to high-tech and foreign-invested enterprises; and the Ring Bohai region, which focuses on application, software, and service-based companies. Together, these regions account for over two-thirds of China's security market. Industry leaders have grown rapidly, leading to a significant rise in industrial concentration. Between 2006 and 2011, the industry's market size expanded from RMB 120 billion to RMB 250 billion, marking an impressive compound annual growth rate of nearly 25%.

Traditionally, security distributors and agents relied heavily on direct sales to end-users. However, in today's evolving landscape, these players are shifting their strategies. A majority—67%—now collaborate with project providers, cutting out intermediaries while improving dealer efficiency. Dealer partnerships account for another 45% of sales, while real estate developers directly engaging with security firms highlight the growing importance of residential projects as clients. Public security agencies, other industry users, and manufacturers also play crucial roles.

China Research Puhua emphasizes that in the face of intense brand competition, larger security companies need to leverage their strengths—branding, service, and pricing—to guide smaller competitors toward a more structured competitive environment. Meanwhile, smaller brands should focus on enhancing product quality, improving customer service, and building their own identities to avoid falling into destructive price wars. China Polytech Industries Research Institute predicts that the security sector will continue to grow, supported by national policies, offering substantial investment opportunities. Extended services and the broader security supply chain are expected to thrive.

The market for China's security industry has seen remarkable growth, expanding from RMB 120 billion in 2006 to RMB 250 billion in 2012, with a compound annual growth rate nearing 30%. By 2011, the market had reached RMB 249 billion, averaging a yearly increase of over 25%. Puhua anticipates the market will double again to RMB 500 billion by 2016, with an annual compound growth rate of approximately 20.24%.

Today, the industry comprises diverse players, including engineering firms, product distributors, manufacturers, service providers, and alarm operators. Statistics show that around 25,000 security companies operated in China in 2010, with fierce competition across all segments. Notably, there are roughly 14,130 security service companies, 1,579 with official engineering qualifications, and 12,551 with local certifications.

The industry’s total output value has surpassed RMB 250 billion, with security products contributing approximately RMB 120 billion and security engineering and services adding another RMB 130 billion. The sector’s added value has grown to over RMB 80 billion since 2005, a 1.8-fold increase. Despite challenges like the global financial crisis and domestic SME financing difficulties, the industry maintains an annual growth rate of around 15%. This promising outlook has drawn increasing interest from both domestic and international players.

As China’s Safe City initiative expands, the adoption of public safety technologies is becoming a global trend. Basic security products, such as doorbells in urban apartments, are now ubiquitous. Urbanization is driving even greater demand for these essential items, making security solutions an integral part of modern living.

As China's "Safe City" initiative continues to expand into second- and third-tier cities, there's been a noticeable surge in global demand for similar public safety projects. Around the world, communities are increasingly relying on advanced security technologies and equipment, making these products more accessible and familiar to everyday life. The report titled "Market Analysis and Investment Direction Research Report for the Security Industry (2012-2016)" highlights that investments in China's urban intelligent transportation systems are projected to hit RMB 127.77 billion between 2012 and 2016, with over 70 billion yuan allocated specifically to video surveillance systems. That averages out to more than 10 billion yuan annually, reflecting the robust demand for security solutions across key domestic sectors.

Over time, China's security industry has evolved into three major regional clusters: the Pearl River Delta, known for its electronics manufacturing prowess; the Yangtze River Delta, home to high-tech and foreign-invested enterprises; and the Ring Bohai region, which focuses on application, software, and service-based companies. Together, these regions account for over two-thirds of China's security market. Industry leaders have grown rapidly, leading to a significant rise in industrial concentration. Between 2006 and 2011, the industry's market size expanded from RMB 120 billion to RMB 250 billion, marking an impressive compound annual growth rate of nearly 25%.

Traditionally, security distributors and agents relied heavily on direct sales to end-users. However, in today's evolving landscape, these players are shifting their strategies. A majority—67%—now collaborate with project providers, cutting out intermediaries while improving dealer efficiency. Dealer partnerships account for another 45% of sales, while real estate developers directly engaging with security firms highlight the growing importance of residential projects as clients. Public security agencies, other industry users, and manufacturers also play crucial roles.

China Research Puhua emphasizes that in the face of intense brand competition, larger security companies need to leverage their strengths—branding, service, and pricing—to guide smaller competitors toward a more structured competitive environment. Meanwhile, smaller brands should focus on enhancing product quality, improving customer service, and building their own identities to avoid falling into destructive price wars. China Polytech Industries Research Institute predicts that the security sector will continue to grow, supported by national policies, offering substantial investment opportunities. Extended services and the broader security supply chain are expected to thrive.

The market for China's security industry has seen remarkable growth, expanding from RMB 120 billion in 2006 to RMB 250 billion in 2012, with a compound annual growth rate nearing 30%. By 2011, the market had reached RMB 249 billion, averaging a yearly increase of over 25%. Puhua anticipates the market will double again to RMB 500 billion by 2016, with an annual compound growth rate of approximately 20.24%.

Today, the industry comprises diverse players, including engineering firms, product distributors, manufacturers, service providers, and alarm operators. Statistics show that around 25,000 security companies operated in China in 2010, with fierce competition across all segments. Notably, there are roughly 14,130 security service companies, 1,579 with official engineering qualifications, and 12,551 with local certifications.

The industry’s total output value has surpassed RMB 250 billion, with security products contributing approximately RMB 120 billion and security engineering and services adding another RMB 130 billion. The sector’s added value has grown to over RMB 80 billion since 2005, a 1.8-fold increase. Despite challenges like the global financial crisis and domestic SME financing difficulties, the industry maintains an annual growth rate of around 15%. This promising outlook has drawn increasing interest from both domestic and international players.

As China’s Safe City initiative expands, the adoption of public safety technologies is becoming a global trend. Basic security products, such as doorbells in urban apartments, are now ubiquitous. Urbanization is driving even greater demand for these essential items, making security solutions an integral part of modern living.

Hot Plate,Electric Hot Plate,Heating Plate,Double Hot Plate

Zenith Lab (Jiangsu) Co.,Ltd , https://www.zenithlabo.com